PCAOB QC 1000 implementation is now an active compliance requirement for PCAOB registered firms that audit issuers and broker dealers, with a compliance date of December 15, 2026. Although there has been public discussion about restructuring the PCAOB, budget pressures, and changes in Board leadership sworn in on February 10, 2026, the text of QC 1000 has not been withdrawn, rewritten, or formally revised as of today.

At the same time, the Securities and Exchange Commission and the PCAOB have signaled a heightened emphasis on prevention through a firm’s system of quality control rather than relying solely on engagement level inspection findings. Under PCAOB QC 1000, inspection focus is expected to begin with evaluation of the design, implementation, and operation of a firm’s quality control system before turning to individual engagement files.

For PCAOB registered accounting firms, the priority should not be speculation about potential regulatory shifts but structured, documented implementation. As part of our Five Points series, here are five questions we are hearing about PCAOB QC 1000 and what those questions mean in practice.

1. Is PCAOB QC 1000 being eliminated or delayed again?

There has been industry discussion about whether the PCAOB Quality Control standard, QC 1000, could be revisited under new PCAOB leadership. However, as of today, QC 1000 remains effective with a compliance date of December 15, 2026, and the prior one year deferral reflected implementation pressure raised by firms, not abandonment of the standard. The requirement for PCAOB registered firms to design, implement, operate, and monitor a system of quality control remains in place. From a regulatory risk perspective, assuming cancellation or further delay without formal action exposes firms to compressed implementation timelines and avoidable uncertainty. Even if aspects of QC 1000 are revisited under new Board leadership, the underlying expectation that firms maintain a documented, risk based system of quality control is unlikely to disappear.

2. How will PCAOB inspections change under QC 1000?

Recent signals from the Securities and Exchange Commission and the PCAOB emphasize prevention through a firm’s system of quality control rather than detection after the fact. Under PCAOB QC 1000, inspections are expected to begin with evaluation of whether a firm’s quality control system is properly designed, implemented, and operating effectively. Engagement file reviews will continue, but increasingly as validation of the firm’s risk assessment process, quality responses, and monitoring activities. This represents a structural shift in PCAOB inspection focus. Rather than concentrating primarily on isolated audit deficiencies, inspectors are expected to assess whether the firm’s overall system is capable of preventing deficiencies. Firms that build disciplined risk assessments, clearly documented quality responses, and ongoing monitoring processes will be better positioned in future PCAOB inspection cycles.

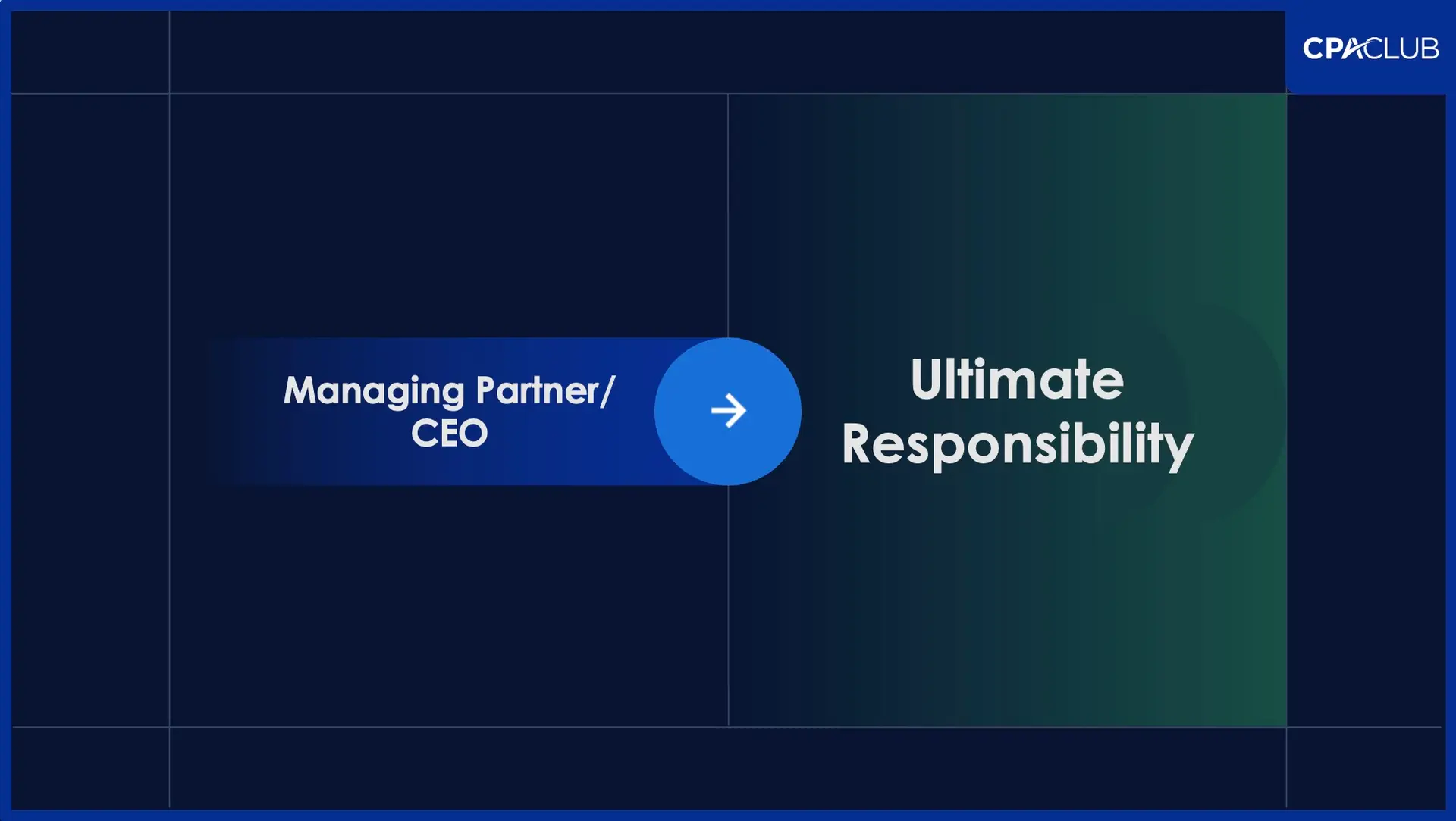

3. What does PCAOB QC 1000 require from managing partners and firm leadership?

PCAOB QC 1000 explicitly assigns ultimate responsibility for the system of quality control to firm leadership, typically the managing partner or chief executive officer, and requires firms to appoint an operational quality leader responsible for day to day oversight of the system. Both individuals must sign Form QC, the annual report on the evaluation of the firm’s system of quality control, certifying whether the system is effective and whether any deficiencies have been identified and remediated. This formalizes leadership accountability in a way prior standards did not. Quality control is no longer solely a technical function within the audit practice. It is a governance responsibility requiring documented oversight, resource allocation, monitoring, and annual evaluation, with leadership certification subject to regulatory review.

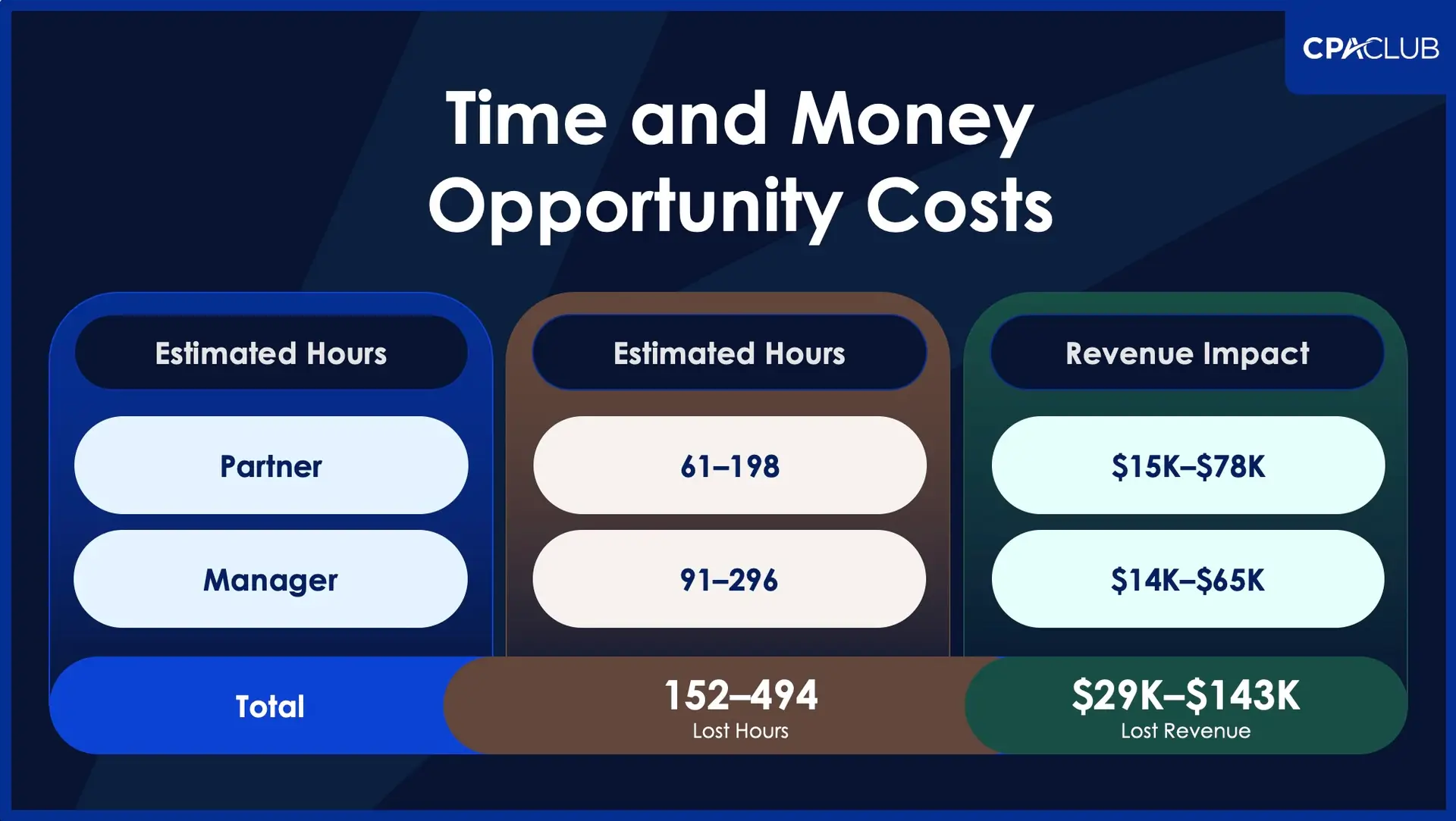

4. How much time and cost does QC 1000 implementation require?

One of the most common implementation questions we receive concerns the time commitment required to comply with PCAOB QC 1000. Firms that have begun implementation frequently report several hundred hours of partner and manager level time devoted to building and documenting their system of quality control.

QC 1000 implementation typically includes:

- Identifying firm specific quality risks

- Designing and documenting quality responses

- Formalizing policies and procedures

- Establishing monitoring and remediation processes

- Preparing for annual evaluation of effectiveness

QC 1000 is not satisfied by drafting a quality control manual. It requires a system that is designed, implemented, operating, and monitored effectively. Without structured planning, firms may experience reactive implementation and opportunity cost pressure. With defined sequencing and clear accountability, implementation becomes manageable and defensible. Quality control implementation should be viewed as a governance investment that reduces regulatory risk and protects long term partner equity.

5. What should firms be doing now with less than a year until QC 1000 compliance?

With approximately ten months remaining until the December 15, 2026 compliance date, firms should be transitioning from design to execution. At this stage, the focus should not be on drafting policies alone, but on ensuring the system of quality control is implemented, operating, and capable of being evaluated for effectiveness.

Firms should prioritize:

- Completing and documenting a firm specific QC 1000 risk assessment

- Mapping identified quality risks to clearly defined and operational quality responses

- Assigning and documenting leadership responsibility, including oversight roles

- Implementing monitoring and remediation procedures that are functioning in practice

- Preparing for the annual evaluation of effectiveness and Form QC certification

This is no longer a theoretical exercise. It is an operational one. While regulatory environments can evolve, inspection expectations rarely retreat. Firms that ensure their system is functioning in practice, not merely documented, will be positioned for regulatory scrutiny under any structure the PCAOB ultimately adopts.

Conclusion

PCAOB QC 1000 implementation is no longer theoretical. It is an active compliance requirement for PCAOB registered firms that audit issuers and broker dealers. With roughly ten months remaining until the December 15, 2026 compliance date, firms should focus on execution, monitoring, and leadership accountability rather than speculation.

CPAClub works with accounting firms to strengthen quality management systems while improving operational efficiency and inspection readiness. If your firm is navigating QC 1000 or the AICPA quality management standards, we encourage you to explore our Guide to Navigating the PCAOB and our Guide to Navigating the New Quality Management Standards. Both provide structured insight to help your firm move from documentation to defensible execution.